Other parts of this series:

In my last post, I talked about the importance of identifying and measuring the right key performance indicators (KPIs) to track the success of Open Banking initiatives. We introduced the various forces that have contributed to the capabilities a bank needs to deliver successful outcomes from its Open Banking initiatives.

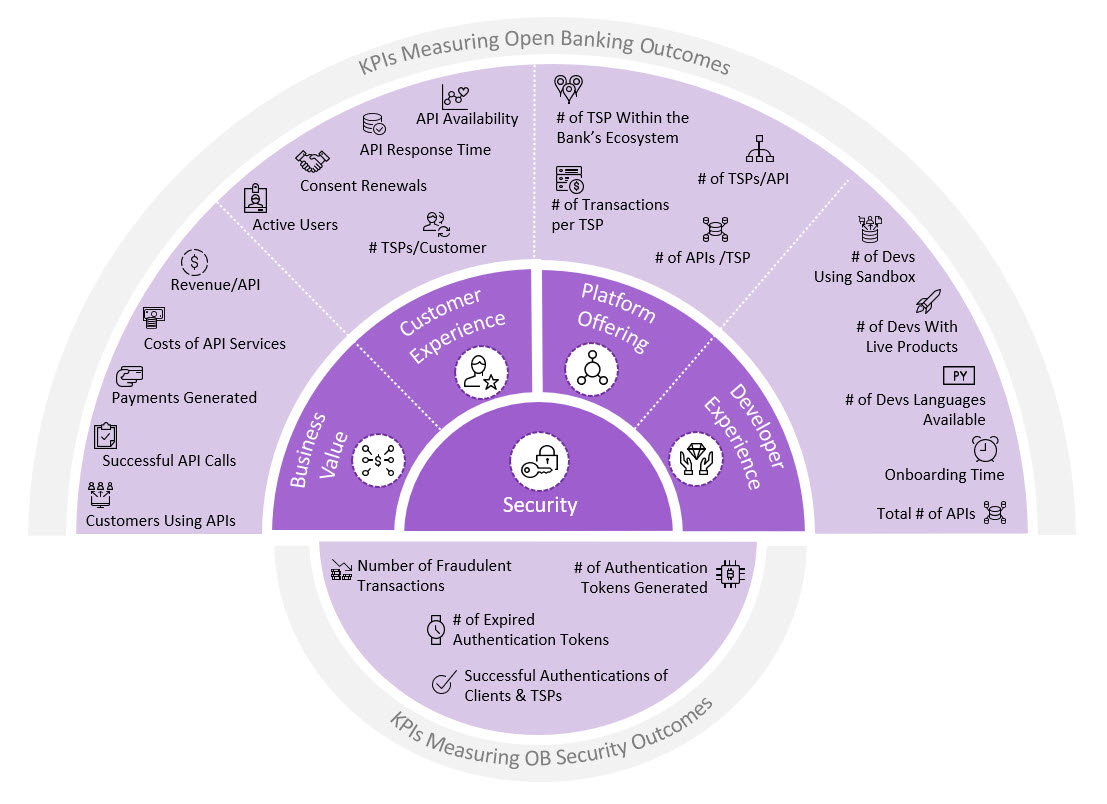

Today, let’s focus on some of the specific KPIs that banks should be measuring across two Open Banking outcomes: business value and customer experience.

Tracking the business value of Open Banking

When it comes to tracking the business value of Open Banking initiatives, banks need to focus on KPIs that measure value created for both themselves and third-party service providers (TPPs).

These are the top six business-value KPIs for banks:

- The revenue generated by each application programming interface (API). This helps the bank understand which APIs are being used actively by customers and which may have the potential to yield more benefit. Tracking which APIs generate the most revenue can influence the bank’s allocation of resources and its partnership strategies.

- The costs of providing API services. Banks should expect the initial costs related to the building and integration of APIs to be relatively high. However, these will fall to a lower, steady level once ‘business as usual’ has been achieved.

- The payments generated by each TPP and customer. The number and value of payments will give banks an understanding of how extensively customers and TPPs are utilizing the services they offer.

- The comparison of payments generated by payment-initiation service providers vs. those for traditional services. Banks should expect this ratio to rise as more customers and TPPs engage with the ecosystem of services and products.

- Successful and/or failed calls per API. This KPI will reveal how successful TPPs are at retrieving information from the bank. A low value may indicate technical issues that need to be addressed. For example, in the UK we currently observe this KPI to vary between 90 and 99 percent.

- The number of customers using APIs. This will help banks to effectively design their API platform and ensure the right performance levels. High traffic to APIs can present challenges to maintaining stability.

To measure success on their side, TPPs should monitor these factors:

- Revenue generated through bank APIs. This will help TPPs to focus on the most profitable bank partnerships.

- Costs related to using API services. Costs will vary depending on the API monetization model negotiated (flat rate, tiered, etc.) TPPs should have a clear understanding of the costs associated with developing an API connection or service.

- The number and value of payments generated per customer. These depend on banking partnerships and the portfolio of digital products. TPPs should focus on the partnerships that create the highest value as well as those in which they can observe significant growth.

- Successful and/or failed calls per API. This KPI shows whether the TPP is providing the right request information.

- Monthly active users. This is a common metric for measuring the success of applications. TPPs should always measure and understand how introducing banking APIs to their customers impacts their active usership.

As Open Banking apps, initiatives and APIs gather momentum, a new Accenture report details how banks can lead in the open data economy.

LEARN MORETracking the customer experience for Open Banking

Customer-experience KPIs are slightly different than business-value KPIs.

The top three that banks should track and measure to enable the improvement of customer journeys and tailored offerings are:

- Monthly active users. Banks, similar to TPPs, need to know how the engagement of their customer base has changed since the introduction of Open Banking services and third-party integrations.

- Consent renewals. This is a key metric that helps banks understand customers’ preferences. Banks can easily identify customer perspectives on which services they deem to deliver high or low value to them by measuring the volumes of consent renewals for these services. They can look for patterns and assess operational challenges, consent processes and the impact of customer experiences on renewals.

- The number of TPPs used by each customer. This reveals whether the bank’s customers are finding TPP products and services attractive. It also shows the level of digitization of the bank’s customers.

Tracking these business-value and customer-experience KPIs and how they impact macro KPIs will enable banks to properly adjust and develop their Open Banking initiatives to meet the rising expectations of customers and stave off the competition from savvy new entrants to the market.

Next time, we will identify specific KPIs that banks should be tracking across three other Open Banking outcomes—developer experience, platform offering and security—that will help banks realize their larger business objectives.

For now, read our report to learn more.