Other parts of this series:

As you start strategic planning this August, consider this: automated, data-driven lending is no longer a future vision—it’s happening now. In our Commercial Banking Top Trends for 2024, we spotlight this critical trend shaping the industry’s future.

This three-part blog series looks at the future of lending, reflecting on industry experiences and providing insights into its transformative power. We explore how banks can use fragmented digital banking models, enhance customer experiences, forge ecosystem partnerships and leverage advanced digital technology to move from defending market share to achieving substantial growth. We outline strategic shifts to drive growth in lending over the next five years and will provide real-world examples throughout. But let’s start by anchoring on the key disruptions happening in lending.

Disruptions in the lending space

Lending is experiencing a remarkable transformation, driven by a convergence of technological innovations, evolving consumer expectations and dynamic changes in the global economy.

- Customers are demanding more seamless and personal experiences, prompting lenders to mirror bigtech in how they reimagine user interfaces, enhance transparency and use customer data for personalized credit.

- Digital advances, powered by AI, data analytics and composable technology, are reshaping loan origination, enabling hyper-personalized offerings, revolutionizing risk assessment and streamlining servicing.

- Regulatory frameworks are adapting, amid this evolution, to accommodate emerging models while safeguarding consumer interests and responding to regulator demands.

- Bigtech’s innovative lending models, targeting billions of users, pose a systemic threat to traditional lenders. Giants like Amazon, Meta, Apple, Google and Alibaba are leveraging their vast user bases and technologies to offer personalized lending models and products ranging from personal loans to futuristic digital real estate mortgages. For example, Amazon has integrated its Sellers Central portal into its quasi-bank, offering personalized business loans to 1.7 million businesses based on real-time sales data.

These forces create a dynamic environment where collaboration between traditional lenders and agile fintechs can revolutionize the way individuals and businesses access capital. The future promises speed, accessibility and customization, where borrowing and lending are seamlessly integrated into the fabric of our digital lives.

So how can banking leaders achieve this vision? We recommend six key shifts:

- Digitize the end-to-end origination experience

- Fuel data-driven lending with a digital brain

- Embed finance into the customer journey

- Take full advantage of sustainable finance and green loans

- Reimagine product and service offerings

- Transform the lending business model

Shift #1: Digitize the end-to-end origination experience

Digital loan origination that combines data and AI can unlock the potential for instant decisioning and disbursement. The origination journey is being transformed by technologies that include workflow orchestration tools, hyper-personalized virtual assistants in the value chain and most recently, generative AI. It’s like giving your loan application a turbocharged GPS with AI—faster routes, fewer bumps and always knowing where you’re headed!

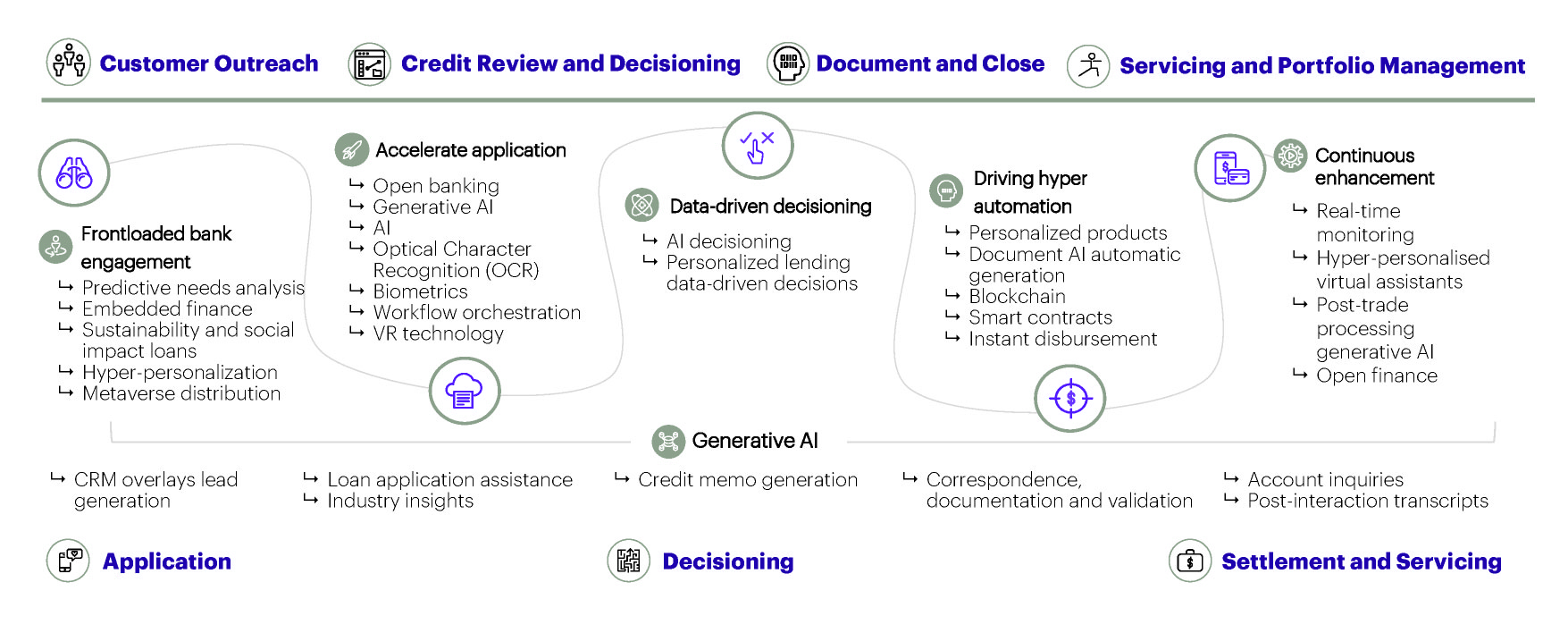

Lending origination journey from customer outreach to servicing and portfolio management

By digitizing end-to-end, banks can create a streamlined and robust experience for borrowers, ensuring a seamless journey at each stage, from application to approval. For example, a South American bank has effectively used advanced technologies such as AI, machine learning and data analytics to transform and digitize an end-to-end auto loan process. They developed a digital platform that lets customers apply for a car loan directly from their car using a mobile app – and they only need to input seven pieces of information. Customers quickly find out if they are pre-approved and learn the maximum loan amount and terms. This use of technology shifts the loan approval process to the start of the car-buying journey, making it faster and easier for dealers to sell cars.

Some banks have chosen to innovate in critical parts of the value chain. A large North American bank is using transaction history, firmographics (firm demographics), revenue and product utilization data with machine learning models to provide relationship managers with the next-best conversation prompts embedded within the CRM platform. Rich Data Corp (RDC), an Australian Fintech working with Australian and US banks, uses banking transaction data sets to provide real-time early warning signals. This provides continual monitoring and detection of potential risks up to 6 months earlier using predictive analytics.

But the future of lending involves more than digitizing the journey. In the next post, we’ll cover three more shifts that cover data-driven lending, embedded finance and green loans.

In the meantime, if you’d like to know more about automated, data-driven lending, we recommend our recent report: Commercial Banking Top Trends for 2024. Feel free to contact us—we’d love to discuss your bank’s journey to the future of lending.

We’d like to thank our colleague, Gustavo Pintado, for his contribution— he works closely with many of our financial services clients as they develop and implement their lending strategies.

This makes descriptive reference to trademarks that may be owned by others. The use of such trademarks herein is not an assertion of ownership of such trademarks by Accenture and is not intended to represent or imply the existence of an association between Accenture and the lawful owners of such trademarks.