How loyal are your customers? And do they feel truly rewarded for their ongoing relationship with your bank? According to recent Accenture research, banking customers view loyalty as a two-way street: they are open to being loyal to one primary bank, but they want their bank to recognize and reward this loyalty. And while the majority of banks claim to be customer-centric, less than 15% actually reward customers for their holistic relationship with a bank.

Accenture’s latest Global Banking Consumer Study of 49,000 consumers in 33 countries highlights what banking customers want from their banks and their growing appetite for new services. Our research shows customers have positive but shallow levels of satisfaction with their main bank. And, after years of stagnation and limited innovation, the banking industry has entered the perfect storm as rate hikes and changing regulations are stimulating bigger changes in customer expectations and trust in their bank than ever before.

Despite active interest, banks are not responding by rewarding customers for their loyalty. As customers are now evaluating the relationship they have with their current bank, banks have a golden opportunity to deepen engagement through integrated products and services, and to truly reward customers for their relationship across the bank.

With this potential on the horizon, banks have a choice: invest now or pay later as customers look elsewhere for banking products and services. How can banks act now to deepen engagement through integrated products and services? And how do they need to evolve to reinforce loyalty among the next generations of banking customers?

Fragmentation and its impact on banking

When our survey respondents were asked about specific aspects of their bank’s offerings, only 23% rated their bank highly for its range of products and services. And just 30% scored their bank’s customer service at least nine out of 10. As a result, customers are more likely to split their banking products across multiple providers—a trend that is intensifying.

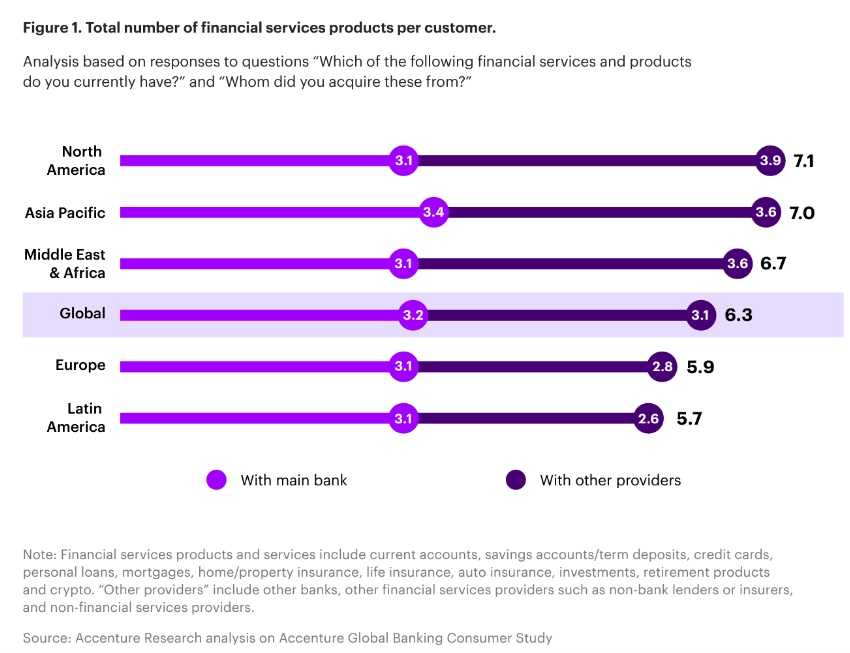

According to our survey, low levels of satisfaction contributed to customers subscribing to products from new providers. In fact, 59% of customers acquired a financial services product from a new provider in the past 12 months. And customers in our sample had an average of 6.3 financial products, with only half of these provided by their main bank.

Furthermore, the emergence of digital-only banks has changed the landscape, with 52% of customers having a product or service with a digital-only bank (with uptake being much higher in Asia and Latin America than in Europe). Most use their digital-only bank for specific purposes, such as payments or foreign currency exchange.

In order to attract, retain and grow customers in the current environment, banks will need to challenge conventions around organizing and rewarding customer lifetime value. The banks that start investing in integrated product propositions that bundle a series of products around deposit customers to reward customers for total value of all products and services will come out ahead.

Loyalty leaders in a new era of customer rewards

With competitive innovation being constant and the post-digital age making it extremely easy to switch providers, it’s time for banks to reimagine customer relationships and how they reward loyalty. By bundling banking products around customers, banks can establish loyalty that transcends transactional relationships. While this sounds simple enough, only 15% of banks worldwide truly reward customers for their relationships across the bank, integrating their debit, credit and other products.

Our research found that over 60% of banks offer limited rewards, mostly for credit card transactions or having products from two or more categories. Most of these banks reward customers with a very tactical and functional benefit: points.

Shifting from functional loyalty programs to relationship-based programs that have more emotional benefits, banks could take a closer look at today’s loyalty leaders and their integrated product innovation, adopting a reward model that is similar to that of Amazon Prime and many successful travel programs.

Qorus–Accenture Banking Innovation Awards: a global competition showcasing the best new ideas and practices transforming the industry. Discover more and enter your winning innovation:

LEARN MORELet’s start with travel loyalty since it hits close to home for me. After over a decade of work travel, I have achieved lifetime “Ambassador Elite” status with Marriott’s loyalty program, Marriott Bonvoy. The program is designed to reward loyal customers in tiered categories, so the more members stay and spend, the more personalized benefits are unlocked. For me, the benefits of flexible check-out times, personalized services on arrival and complementary room upgrades have made my Bonvoy experiences stand out. As a result, even when it comes to personal travel, I go out of my way to stay at a Bonvoy brand hotel, knowing that my ongoing loyalty will be rewarded. This type of emotional, relationship-oriented loyalty program pays off. And many agree with me. Following the launch of the program, 52% of room occupants worldwide were Bonvoy members.

Continuing to look outside banking, the communications and technology industries are also leading with relationship-based programs. In addition to Amazon, Swisscom Blue Benefit bundles products: it offers customers savings when they combine their mobile and internet subscriptions. This approach saw 80% of Swisscom’s broadband connections and 46% of its mobile subscriptions being included in Blue Benefit bundles. Google One also bundles according to the level of a customer’s cloud storage; this reportedly contributed $1.1 billion to the company’s revenue in 2021.

So, what can banks learn from these reward programs? Some are already taking notes and moving in this direction. For example:

- Lloyds Bank’s Club Lloyds is a tiered subscription model that offers lifestyle benefits including streaming subscriptions, movie tickets, dining offers and more. For instance, members receive credit interest if they set up multiple direct deposits / automatic transfers from their account. Ultimately, this increases the amount members are likely to deposit into that account and rewards them for it. Today, Club Lloyds has over 1.6 million members whose average deposit balance is 2.7 times greater than that of non-members.

- DBS Multiplier Savings Account offers bonus interest for customers who connect data from other banks. Additionally, the bank rewards customers for monthly transactions (>$2,000) across eligible products and for spending a certain amount monthly through the DBS super-app PayLah!

- Bank of America created an offering along the lines of Amazon Prime to increase retention. It achieved a 99% retention rate and doubled the number of products held by the average program member.

My colleague, Michael Abbott, also recently highlighted the need for this type of integrated proposition and discussed the ways banks can grow through customer relationships. This is a critical topic today, and banks that move now to create meaningful product bundles will be better positioned to deepen relationships for growth. And as customers compare their loyalty experiences to those of non-banking brands, they will expect their banks to meet ongoing loyalty standards similar to hotels, Amazon and more.

Building the onramp early

The next generation of customers are rewriting the rules of brand loyalty, and this will fundamentally change the way they engage with their bank. I’m always intrigued by how the younger generation is bringing change to the industry and our report’s insights into their expectations are compelling evidence of the need to act now. It shows how this generation is more than willing to switch banks when they’re not satisfied and will readily choose non-bank options. And, with an estimated $60 trillion expected to be passed on to Gen Z and Millennials as inheritances over the next 25 years, banks need to adapt to meet the needs of today’s youth and establish loyalty early.

Today’s youth are growing up in a much more complex world than that of their parents and the generations that came before. They are highly tech-savvy and susceptible to social media and other societal pressures. And they will learn to flex their financial independence through new channels, digital currencies, social platforms and experiences.

Younger customers seek authentic experiences from their banks, and want to collaborate with brands instead of being marketed to. The evidence can be found in the growing reliance on ‘finfluencers’ on TikTok, YouTube and Instagram for financial advice. As young customers are critical of marketing tactics, finfluencers are already embedded in their social lives and represent more authentic connections. Banks must learn from this and collaborate with the younger generation to build connections with trust, leaving the more traditional marketing methods behind and rewarding young customers for their relationships.

Finfluencer: noun. A social media influencer who gives advice on financial investments.

To explore this topic more, I’ve invited two respondents to share additional insights into their generation’s expectations around customer experience. Let’s hear more from their perspectives.