Other parts of this series:

Accenture’s four-part framework for digital fluency predicts 54 percent of a worker’s ability to be agile. Learn why technology, skills, operations and culture are essential to achieving digital fluency—and the competitive agility it enables.

As I introduced in my previous blog post, digital fluency is essential for banks’ performance in the near-term (to support remote and hybrid working) and long-term (to unlock the full benefit of digital transformation).

But what does it look like in practice?

We worked with a large European bank to support its pivot to learning in the new by helping it change how people learn and work, with digital at the heart.

- An in-house media agency—a learning lab—delivers more than 300 learning objects per month, 70 percent of which are video-based. It means pulling on design thinking and agile, storytelling and investing in specific technologies to support high-quality media production.

- The data-driven approach enables the team to monitor production costs and timing, define new use cases and track success, and use AI to make learning more effective based on employees’ needs.

- A mobile learning experience is tailored for employees to get personalized recommendations for adaptive and contextual learning; management gets specific features like coaching. In addition, the Italian bank can sell its learning contents to mid-size banks to generate additional revenues.

Over a multiyear partnership, we worked with the bank’s HR directors and a digital oriented Learning Officer to transform the entire learning experience and increase people’s digital fluency:

- Innovative: Launched a new learning service that is flexible, personalized, user-friendly and easily accessible.

- Effective: Delivering 300 learning objects per month, with more than 2 million views in one year; more than 80 percent of commercial banking products and services are covered by digital learning.

- Cost-effective: Saved $30M in cost savings in three years.

Overall, the partnership enabled this large European bank to transform learning from a cost to a revenue source—especially because it was able to monetize its learning contents and sell them to mid-size banks. Its focus on digital fluency will enable it to innovate and create a competitive advantage in its market.

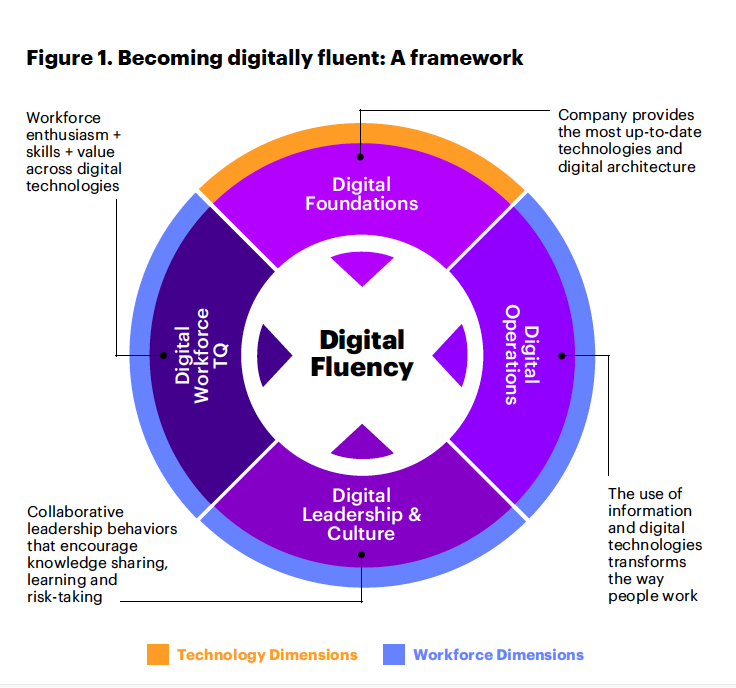

A framework for becoming digitally fluent

That’s an inspiring example that shows the tremendous value that can come from investing in digital fluency. But there is still lots to do. The 2020 Accenture Global Digital Fluency Study shows that just 14 percent of companies are digitally mature—which we define as scoring high in all four components of our digital fluency framework.

So how can you improve your bank’s digital literacy?

- Build a digital foundation

- Improve your workforce technology quotient (TQ)

- Enable digital operations

- Shape a culture of digital leadership

Let’s look at each of these in more detail.

Build a digital foundation

This is the technology side of digital fluency—an essential, but not the only, component. It’s especially important for banks, which face the double whammy of legacy complexity and regulatory challenges. Digital transformation can empower an organization to be more efficient and ready for change, as well as responsive to regulatory changes. It means being able to create new experiences for workers and customers.

For example, cloud supports more flexible and adaptable technology—and that, in turn, enables a business to make quick pivots. We saw many organizations make quick pivots in response to COVID-19, but pivots can also be a response to something desirable, such as a business opportunity, a chance to explore new operating models or to try new ideas. And our research shows that 65 percent of the banking workforce say their employer uses digital tools to promote innovation, collaboration and mobility.

In addition, banks should consider digital adoption—that is, that people actually use the tools they’re offered. Too often, companies mean well by providing new tools, but don’t actually help frontline users see the value of changing their habits to adopt the new tool. Digital adoption platforms like WalkMe provide contextual, personalized guidance to help people get the most from their digital tools: that is, to help people drive the change that technology promises.

A digital foundation supports flexibility. Flexibility enables agility. And agility is essential for business performance today and in the future.

And cloud is just one of the technologies with the potential to fundamentally change how businesses go to market, such as blockchain, 5G or AI. What could your bank achieve at the intersection of some of these technologies? How could you deliver greater value to customers through new business or operating models? How can you enhance the employee experience to help people derive more meaning from their day-to-day lives?

The Chief Information Officer (CIO) plays an important role in enabling digital transformation. We’re also seeing a shift in the CIO’s role. No longer is the CIO a purveyor of services; rather, the CIO is a steward for how technology shapes an organization’s change journey. Think of a CIO as a strategic partner who sets timelines and enables a digital workplace with opportunities for people to enable themselves and automate tasks to free people to work on creative, value-added problems.

Improve your workforce’s TQ

First there was intelligence quotient (IQ), emotional quotient (EQ), and now there’s technology quotient (TQ). This is the skills piece of the digital fluency puzzle, and done well it unlocks workers’ enthusiasm, expertise and value. It is a critical piece of an organization’s digital resilience. Nearly three-quarters (72 percent) of the banking workforce say their employers consider digital skills to be important.

Notably, improving workforce TQ can also tie into an organization’s ESG agenda as it creates societal good. Consider Amazon’s recent announcement to offer free cloud computing training to help 29 million people worldwide.

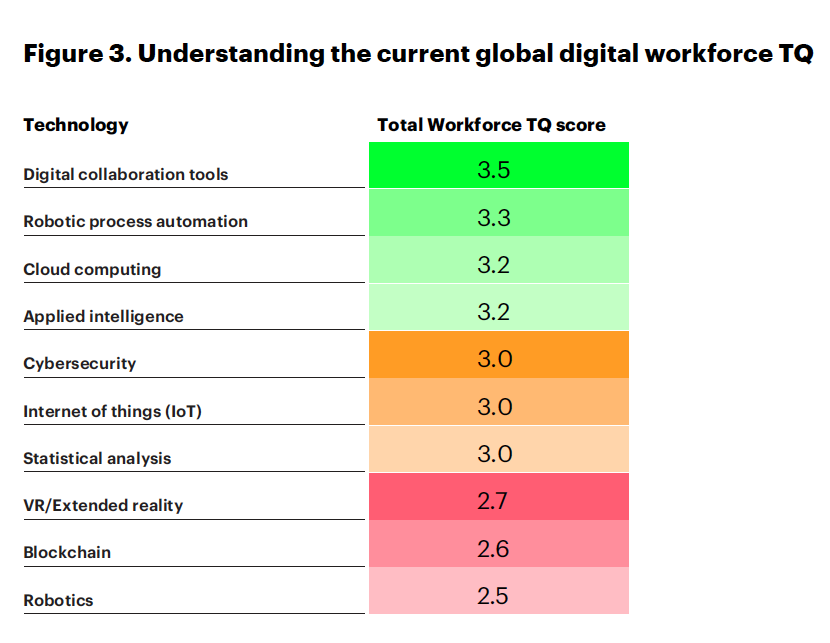

Click/tap to enlarge

Globally, we found that while digital tools and technologies are available to many, many workers lag in their digital skills. For example, when ranked on a scale of 1 (low fluency) to 5 (high fluency), only four skills emerged above the mid-mark. Certainly, digital collaboration tools, robotic process automation, cloud computing and applied intelligence are important—and there are many other skills that workers will need in order to be competitive and resilient.

In banking and capital markets, workers are eager to build their TQ. When asked about technologies that can add value to their job, the top three responses were cyber security (69 percent), digital collaboration tools (66 percent) and cloud computing technology (63 percent). Those three also ranked at the top of technologies that workers are interested in developing skills.

So how do you create and sustain behavior change to support workforce TQ? You need people to have the right attitude (enthusiasm), the right skills (competencies for success) and relevance (to see the value for themselves and the company).

Few digital skilling initiatives account for all three factors of creating sustainable behavior change: attitude, skills and relevance.

In addition, TQ should be embedded throughout the organization—from entry-level hires to the leadership team. It’s not just the CIO who needs TQ, but the entire executive board, and the Board itself. Everyone in the organization needs to stay current—and ahead of current trends.

Finally, developing TQ need not be an arduous process. In fact, the best learning experiences happen when people don’t feel like they’re learning at all. For example, I love this story of PepsiCo using Minecraft to teach people about Lean Six Sigma principles (an idea that came from one employee’s 11-year-old son).

Enable digital operations

Enabling digital operations goes far beyond automation and efficiency—it’s an opportunity to redefine the value chain and reinvent work. Banks need a holistic view of how digital transformation affects their processes and policies, as well as how people work with each other and interact with customers. It’s critical to look at the long-term implications of technologies, like AI, and what it means for the workforce.

Digital operations will transform ways of working, and success relies on helping people understand the value of new technologies—and how they can unlock the future.

Our study of digital fluency in banking and capital markets found that seventy-one percent say their company leverages modern technology architecture to promote speed and flexibility, and 68 percent say their company integrates digital technology into daily operations to enhance performance.

Organizations will achieve success by bringing people with them, to help individuals pivot their work and energy to create new forms of value. This can support meaningful day-to-day work and help people feel like they’re working toward something greater than themselves—a crucial piece of leaving people Net Better Off.

Shape a culture of digital leadership

Finally, banks need to foster a culture of digital leadership. Digital transformation and digital fluency need leadership that is aligned to the goals and culture that enables digital fluency. Among banking respondents, 62 percent said their senior leaders prioritize investment in targeted digital education and training for all employees.

Even before the pandemic, the social, economic and environmental challenges of the 2020s required new approaches to leadership and responsibility. For example, the World Economic Forum (WEF) was founded on the concept of “stakeholder capitalism” and a triple bottom line—and I’m proud that our continued partnership with WEF enables us to focus on how to help business drive social good, achieve ESG goals and address sustainable development.

Responsible leadership requires banks to shape a new culture. Some questions to ponder:

- What should new work structures look like?

- How should roles and responsibilities evolve?

- In what ways can digital enable better knowledge sharing and collaboration?

- How can leaders be trained to communicate better, have greater empathy and earn trust in a remote work environment?

Our survey of US financial services C-level executives found that most banks were prepared for work-from-home in terms of technology, but few were culturally prepared.

As we move toward a future where hybrid workforces (a combination of in-person and remote work) are common, culture becomes essential to innovation and competitiveness. Banks must cultivate an environment and culture for learning and digital fluency, one that embodies a growth mindset, one that is fuelled by curiosity and continual learning.

Psychological safety and trust is essential to allow people to achieve their full potential at work, and in turn, for banks to drive business performance. Consider that our Transformation GPS research indicates that 85 percent of transformations that fail do so because of organisational dynamics, especially due to issues of fear and trust.

Said another way, fear in the workforce inhibits change, and change is precisely what is needed right now.

Baking trust into digital transformation

Digital fluency is especially important on remote teams. If you can’t use the tools, you can’t participate. And if you can’t use them well, you can’t feel engaged, included, trusted, or able to contribute to your full ability.

Digital fluency can mitigate fear and anxiety about workplace change.

Digital fluency can help people see technology change as a way to get more skills, better tools and the opportunity to contribute more. It can inculcate a sense of control and agency that helps people achieve their full potential at work.

For banks, in particular, digital fluency can drive innovation and ethics as people become more competent with tools. The ethics piece is especially important in a regulated industry like banking, as a culture of trust and agency can support people to speak up early, before issues get out of control. This applies equally to regulatory issues like fraud and risk management, as well as to culture and workplace issues of harassment, inequality and bias.

Finally, digital fluency in the workplace can help leaders manage change, be more agile and become more adaptable. It can enable banks to provide more relevant, personalized services to customers, via tools to help them manage finances and improve their life’s outcomes—in other words, to build trust by providing more value.

Digital enables agility

Digital fluency is about overall readiness for constant change. It’s about market preparedness: we know that banks that were digitally ready performed better as COVID-19 hit. It’s also about making specific changes within the organization, whether that’s providing people with new skills to shift into different versions of their roles, or into entirely new roles. And digital fluency is linked to agility, a capability that is more and more important as disruption increases.

The benefits of technology aren’t automatic or equally distributed. The full potential of technology and digital will only be realized by banks that transform their workforce to harness digital fluency.

High performers will be those that take the opportunity to reimagine work and understand how technology and digital can unleash human ingenuity.

How? By equipping and empowering people with four components of digital fluency: tech, skills, operations and culture. By enabling people to experiment and find new forms of value. By embodying a growth mindset, seeing failure as learning, aligning incentives and promotion with innovation and creativity. By scaling up new skilling, and by creating customized and appropriate learning paths according to people’s needs.

Need a place to start? I suggest cloud. It’s been instrumental in banks’ ability to respond to the needs of a distributed workforce. Our research shows that half of respondents in our digital fluency survey are enthusiastic about learning about the cloud and agree that it will be important to their job—but only 35 percent have the skills they need. What’s more, 51 percent of millennials are eager for cloud adoption, which makes cloud something that can help a bank attract and retain future talent. How cloud ready is your organization? Take our quiz for digital fluency for cloud computing (scroll to the bottom of the page).

To learn more about how to improve your organization’s digital fluency, contact me or reach out on Twitter at @andyyoungACN.

Many thanks to Eva Sage-Gavin, Emma McGuigan and David Shaw for your leadership, and Kelly Monahan, Ph.D. for leading the research study.