The COVID-19 pandemic increased the tempo of change in consumer behaviors and expectations. Payments, characteristically, is at the forefront of the change. In “Payments Gets Personal—Strategies to Stay Relevant,” our report on an Accenture survey of 16,000 payments customers across 13 different countries, we revealed how the return of meaningful interest rates is interacting with ongoing digital disruption in payments to reshape the expectations of customers. We also discussed the viable strategies for payments players.

This is what we found.

Next-gen payments rails grow as consumers seek more control

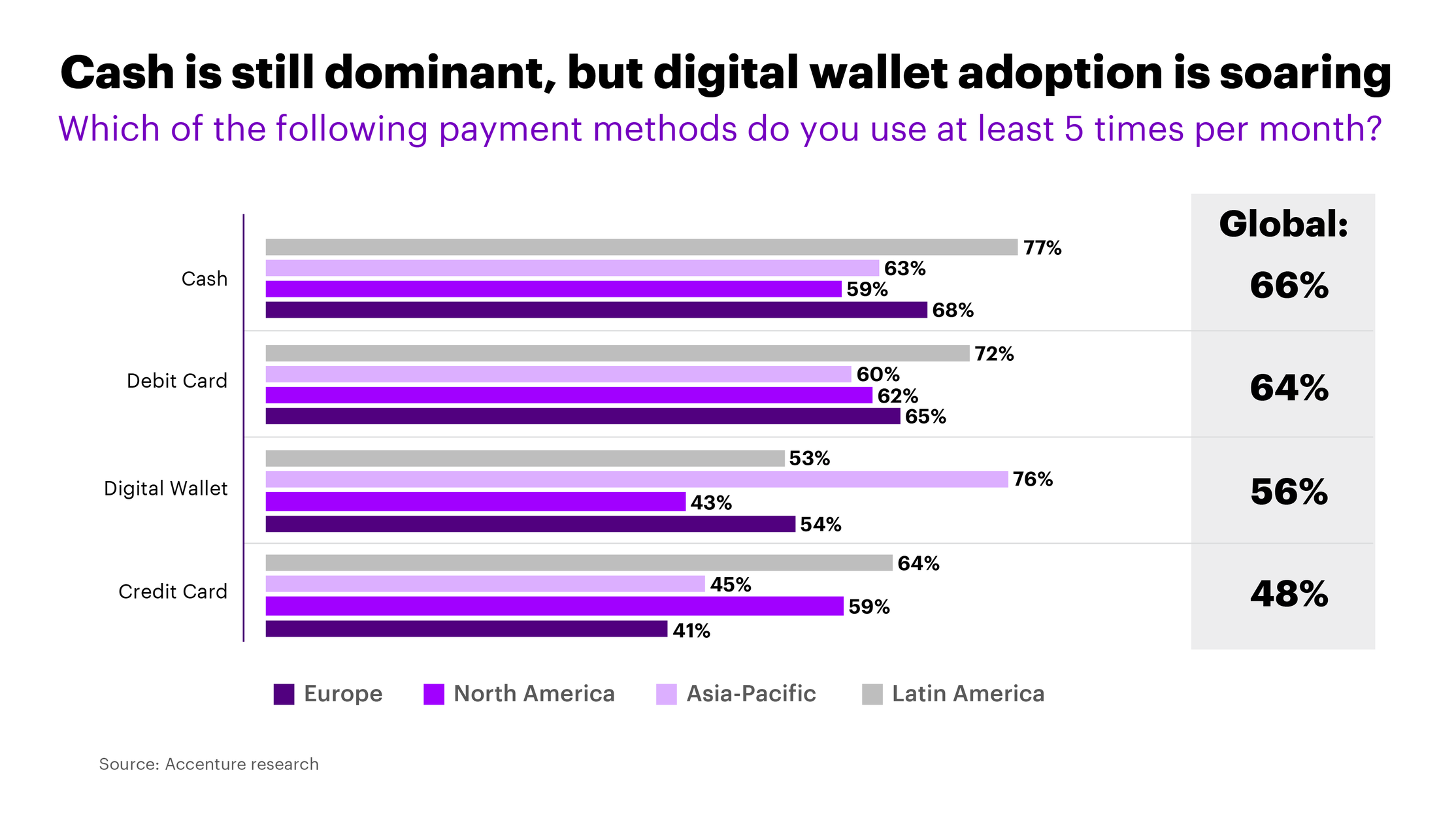

One of the survey’s most interesting findings is that digital wallets are more widely used than credit cards. Specifically, we asked customers to list the payments methods they use at least five times per month. Well over half listed digital wallets, compared with 48% for credit cards.

Some consumers also told us they use other next-gen payments options at least five times a month. Account-to-account payments (A2A) was mentioned by 10%, while 6% included BNPL.

These are not the only next-gen payments tools growing in popularity. Our research also found that 56% of consumers want a single app for all payments and 60% want a single app to track payments from all payment providers.

There are only a handful of true super-apps on the market today, most of them in the Asia-Pacific region. But our research suggests that the time of the super-app may be at hand in other markets too. This is reflected in the growing number of organizations moving towards becoming super-apps, including PayPal, Revolut and even Twitter.

What’s driving the popularity of these payments methods? Economic uncertainty is growing due to inflation, rising interest rates, the war in Ukraine and recent concerns about the liquidity of some banks. That’s creating a widespread desire for control among customers—and next-gen payments options are better able to satisfy that desire than some other options.

And so can cash. Our research found that it’s still the most frequently used method of payment, with 66% of global consumers using it at least five times a month.

The connection between economic uncertainty and the demand for control over payments methods is neatly captured in what one UK respondent told our research team:

“I‘ve stopped using my debit card as much and I’m using cash just to be able to budget easier, feel more in control, less tempted to overspend. I can only spend what’s in my purse, so I don’t go looking around for little extra treats to give myself.”

While this customer turned to cash to manage and limit spending, many next-gen payments include powerful tools for tracking and control. The common thread is that today’s consumer expects personalized payments options that empower them to manage their own spending.

For payments providers and merchants, that means offering a wider range of payments options than ever.

Trust remains an advantage for banks—but it’s not enough on its own

Our research also found that banks are still the most trusted providers of secure environments for financial transactions. No fewer than 84% of consumers trust their banks to manage their payments securely, compared with just 47% for big tech firms.

In past times of economic turmoil, this trust edge has been an important competitive advantage for incumbents. Our research confirms that the edge abides—but our findings also suggest that trust, on its own, will be no guarantee of payments success or even relevance in the future. Customers are clearly willing to try alternative service providers in the payments space, especially when they are frustrated with the experiences incumbents offer.

We asked consumers for their top payments pain points. The five most common answers, in order:

- Slow payment experience (19% of respondents)

- Payment gets declined or tap-to-pay does not work (13%)

- Merchants don’t support my preferred way of paying (11%)

- Can’t link my card to my digital wallet (7%)

- Cumbersome online credit card process (6%)

The main takeaway from this is that customers seek payments experiences that are seamless but still offer control.

Powerful ideas for payments growth in 2023

Our analysis confirms that the stakes are high for incumbent payments providers in today’s market. Those that fail to keep pace with disruption or to invest in next-generation payments options could, together, lose as much as $89 billion in revenue between now and 2025.

That’s why we also identified four strategies that can be used, alone or in combination, to protect and grow your payments business.

|

Partner to scale: The right partnerships offer the promise of rapid scaling and adoption of next-gen payments solutions. The keys to success are simple customer journeys and finding the right partners. Notable examples of the results this strategy can produce include the Zelle peer-to-peer money transfer app in the US and the Blik account-to-account payments system in Poland. |

|

Use technology to boost simplicity and speed: Most incumbents have already deployed apps and digital wallets that simplify and accelerate routine transactions. Further gains are likely to come through strategic investment in technology like AI and the cloud. |

|

Develop a niche focus: A tight focus on particular products or customers can distinguish a payments brand. Success here will require a deep understanding of customer requirements and the right partnerships. |

|

Look beyond payments: Online marketplaces and super-apps can move payments players towards the center of their customers’ digital lives. This will require dynamic use of data to understand and respond to customer requirements. |

Payments players today walk a delicate line between protecting their existing revenue streams and capitalizing on new opportunities. At the same time, customer behavior is evolving rapidly and new competitors are emerging to quickly meet any unmet demands. Our global consumer payments research is packed with important insights for any payments player looking to compete in this dynamic and challenging space.

Read reportTo discuss how your payments organization should respond to the changing demands of today’s consumer, contact me here.