When it comes to whether emerging technologies like artificial intelligence (AI) and blockchain are practical for equipment finance, it depends on the application. That was the key takeaway from the recent ELFA 2020 Business Live! virtual convention panel discussion I had the fortune of being a part of.

I joined host Deb Reuben of TomorrowZone and fellow panelists, Jillian Munson of QuickFi and Erich Dylus of Vedder Price for a one-hour discussion about how some of the most disruptive technologies—AI and machine learning, distributed ledger technology (or blockchain), the Internet of Things (IoT) and biometrics—can and are being applied in equipment finance and other industries. Here, I’ll summarize some of the key points.

AI & Machine Learning: Lenders are skimming the surface

Equipment finance organizations are just beginning to realize the potential of AI and machine learning. In Accenture’s Tech Vision for Equipment Finance report, 93 percent of equipment finance executives claimed their organizations are piloting or adopting AI while only eight percent say they’re preparing their workforce for collaborating and interacting with AI.

While there are some who view AI, machine learning or automation as replacements for people, I think the future of these technologies is collaboration, how humans will leverage them to do their jobs better. A great example was how banks and captive finance organizations used AI bots to deflect calls when they were inundated during the first onset of COVID-19. Many callers were able to complete their transaction with bots, enabling greater call efficiency and service.

There are more use cases for AI and machine learning in equipment finance beyond call deflection, though. AI is also being deployed to analyze vast amounts of data in order to streamline customer acquisition and improve retention as well as increase the value of assets.

Distributed Ledger Technologies: Both hype and reality

The results from the audience poll asking whether distributed ledger technologies were hype or reality were telling: More than a third of respondents said they were both.

Distributed ledger technologies, or blockchain, are best known as the technology underpinning cryptocurrencies like Bitcoin. However, this technology has many more potential uses, some of which are already in play. Smart contracts have obvious applications for lenders and customers who want immutable, decentralized contracts and who want to remove middlemen. There are also applications for storing electronic signatures and other documents on the blockchain. QuickFi stores equipment finance contracts on the Ethereum blockchain for better accessibility and security.

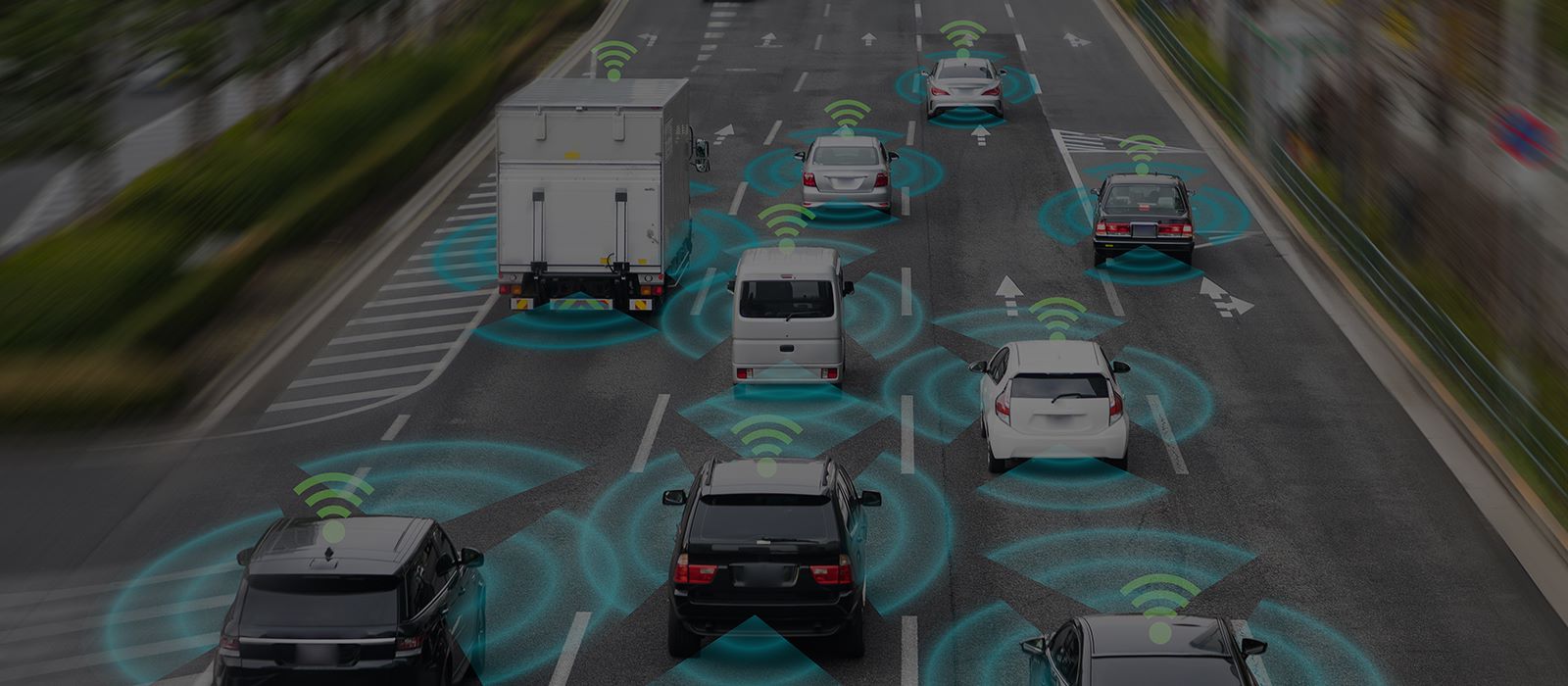

Internet of Things: Real and growing exponentially

Seventy percent of the audience said they see real applications for IoT in equipment finance. According to Statista, the IoT market is expected to grow by 75.44 billion connected devices by 2025. There is so much data and the problem is that we don’t know how to handle it all…yet.

IoT has been around for quite a while in equipment finance. Remember that copier you used in the late 1980s with the modem that connected to the wall and communicated when it needed service, paper or toner? IoT has expanded significantly since then, to connected vehicles, for example—not just cars, but tractors and railcars too—and with that comes a lot of valuable data. Companies that monetize this data will become leaders by learning more about what their customers want and tailoring experiences for them. For example, lessors can proactively maintain equipment or suggest upgrades close to the end of a contract.

There’s also the case of zero-dollar finance contracts, which we’ll see first in the autonomous mobility market. Imagine free rides from companies when you willingly share your internet search data.

Biometric Identification: Adoption is already there

It was interesting that no one in the audience though biometrics were hype. We’re used to unlocking our smartphones with our thumbprints. For equipment finance organizations, biometrics can help reduce fraud and aid identification verification, speeding up KYC processes for businesses and information access for customers. Combined with e-signatures, biometric identification is more efficient and secure than passwords, which can be easily lost, forgotten or compromised.

Of course, the issue with this kind of data combined with the enormity of IoT is security. When will the data be used and when and how will it be deleted? Blockchain could aid the solution here, giving individuals more control over where and how their identity data is used. This is where companies need to look at their collection of services instead of focusing on the hype around any one technology. Integrated, biometrics, the IoT, blockchain and AI can help companies develop novel and responsible solutions to innovate and improve the customer experience.

Where do we go next? Companies that fold continuous innovation into their organizational DNA and place the customer front and center stand to benefit significantly from emerging technologies. It comes down to understanding needs—yours and your customers’—and building solutions that address them.

Learn more about the impact of emerging technologies in equipment finance in Accenture’s Tech Vision for Equipment Finance report.