Consumers want more options—payment choices included

As consumers experience economic turbulence due to inflation and rising interest rates, they want to be able to pay anywhere, anytime, anyhow.

For banks to stay ahead of an increasingly complex payments game and meet these evolving consumer expectations, they will need to innovate and seize emerging opportunities. One opportunity we’re watching closely is BNPL (buy now, pay later).

Our 2022 Global Consumer Payments Survey—of which this report is an extension—found that consumers, on average, expected to double their usage of BNPL for online payments in the next three years. Further, four in 10 would be more willing to adopt BNPL if it were provided by their primary bank.

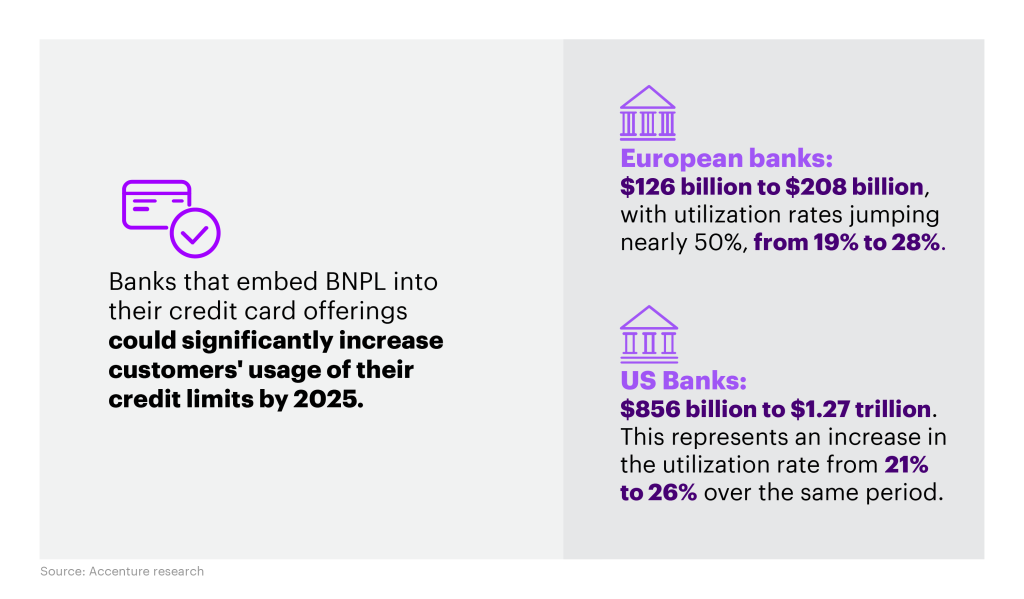

In addition to helping banks defend their consumer finance and credit card businesses from new competition, BNPL could offer banks a significant growth opportunity.

Where can banks offer value in the BNPL space?

Banks can emulate the "anywhere, anytime" experience offered by independent players and offer customers a more frictionless experience with instant approvals and added convenience.

When offered by the consumer’s trusted financial institution, BNPL could represent a convenient alternative financing option, with the ability to trace transactions and manage repayment more easily through banks’ existing financial wellness tools. The use of data, cloud and artificial intelligence in this space will empower banks to go beyond today’s offerings and comfortably manage any regulations, should that become necessary.

Two scalable BNPL plays for banks

Success in the BNPL boom will require banks to evolve and embed BNPL into their existing propositions and platforms to capitalize on the issuing and acquiring opportunities.

There are two strategic plays for banks to consider:

- Follow the customer: The cardholder or borrower decides with which merchant they want to use BNPL.

- Follow the seller: The proposition is aligned to a single merchant or category.

In exploring strategies now for BNPL success, banks can chart their paths forward to create multi-dimensional value. Attention and effort should focus on creating lifetime value and becoming a more important financial partner to both the customer and the merchant.

Author

Dilnisin Bayel