Other parts of this series:

In part one of my blog, I explored how current macroeconomic events are akin to a solar storm and the Northern Lights are the manifestation of the banking industry’s reaction to uncertainty. In part two, I will discuss key areas banks should focus on to avoid becoming paralyzed by the challenges they face.

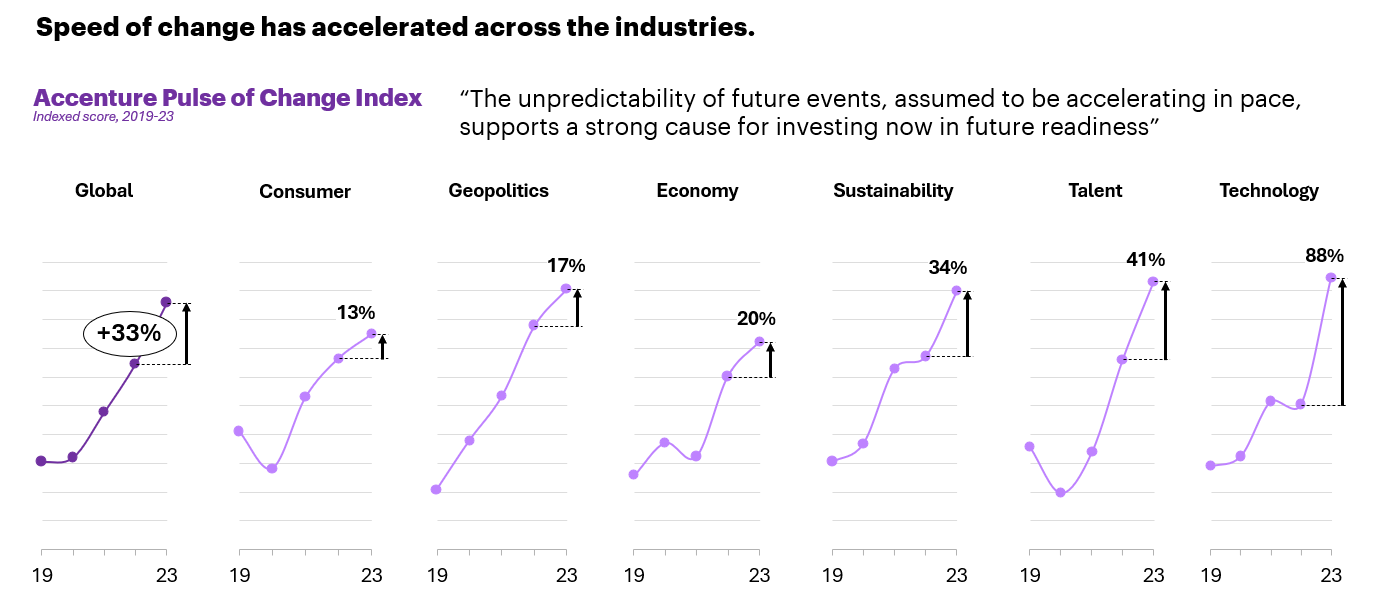

Over the past 18 months, once clear message has emerged: unpredictability is persistent. The era of low rates and predictable macroeconomic forces has ended. I believe that our economic cycles—including rates, inflation and credit quality—will only continue to evolve with greater pace. The unpredictability of future events, assumed to be accelerating in pace, supports a strong cause for investing now in future readiness (see below). Adopting flexible technology and a scalable operating model will be crucial for quickly adapting to the accelerating pace of economic changes.

Balancing the books: Prioritizing financial health in rapid economic shifts

In order for banks to prepare for accelerated economic cycles, banks need to prioritize their balance sheets. After years of cheap capital, low deposit costs and stable credit quality, these standards are under pressure. Banks should look to shield their operations from the harmful radiation of the “solar storms” by focusing on managing interest rates and credit risks effectively.

Interest rate management

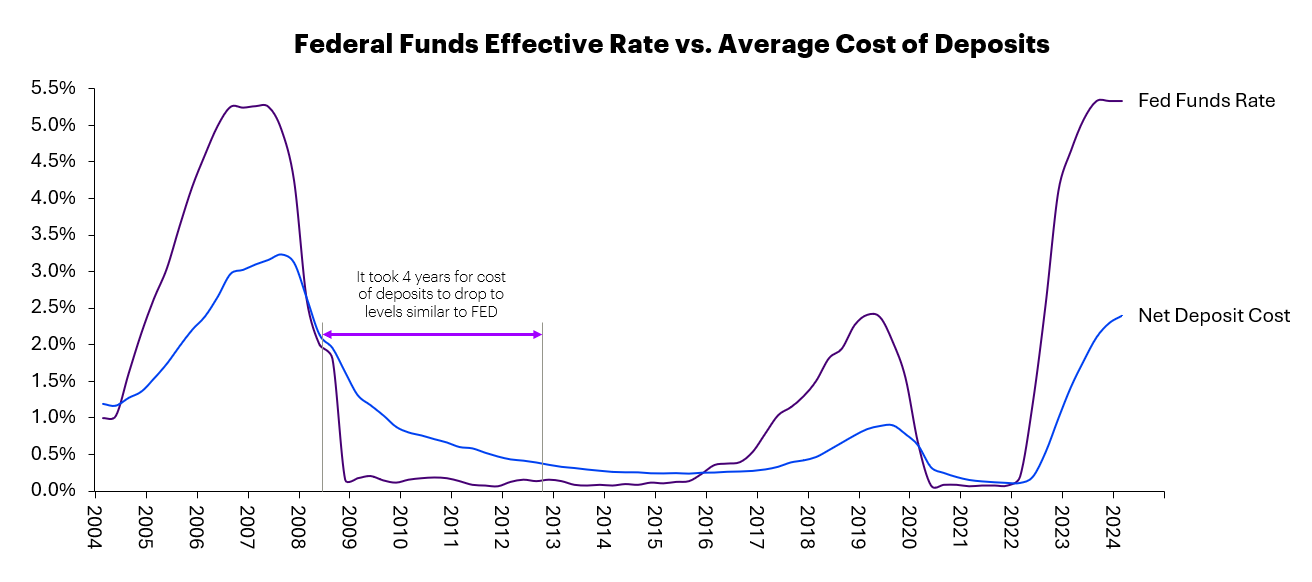

During the last period of declining interest rates from 2008 to 2012, it took banks nearly four years to adjust their deposit costs to match the federal funds rates. While my previous blog discussed how banks should capitalize from higher profits when rates increased, now they need to focus on deposit management to get ahead of potential losses when rates are expected to fall. Banks took the opportunity to gradually increase their beta to sustain profit margins as rates rose. However, reducing the deposit rates they offer customers too swiftly to match decreases in the FED funds rate can lead to the risk of customers moving their money elsewhere.

Credit risk

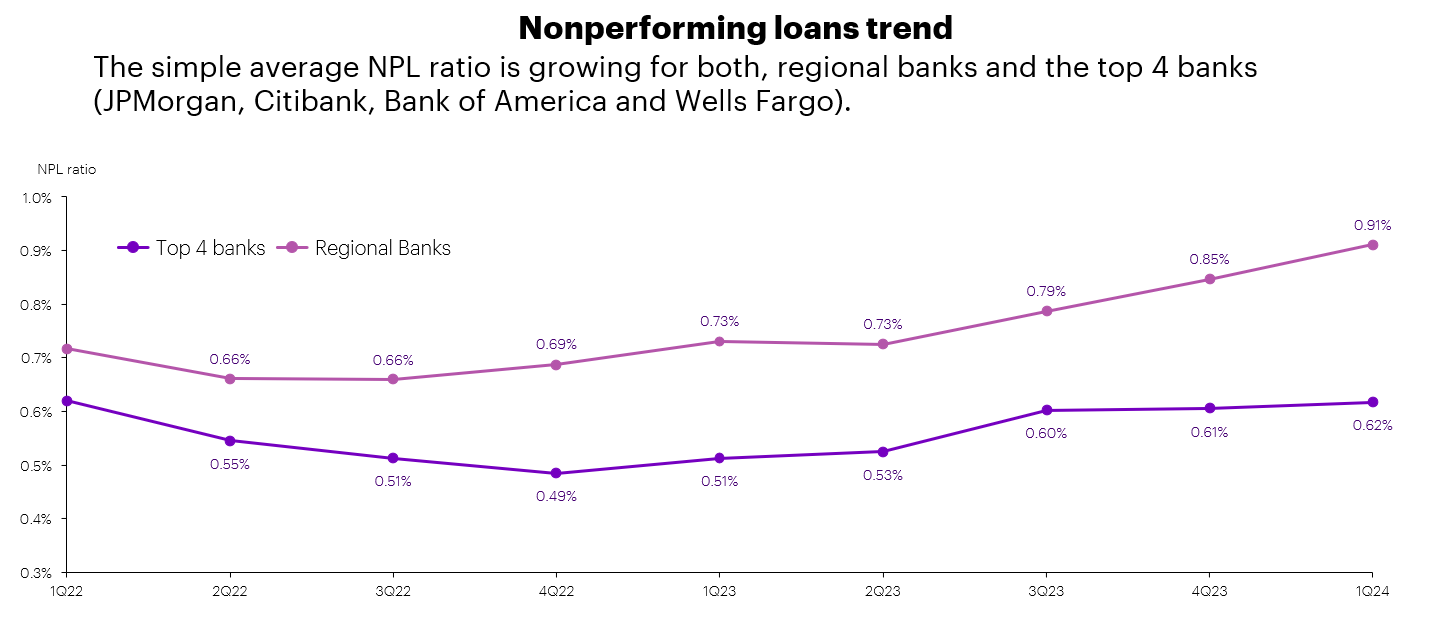

As customers of retail banks have used up their savings from the pandemic and started using credit to cope with rising prices, the quality of credit in the industry has declined. Non-performing loans are on the rise with provisions as a percent of revenue at 9.5% (avg non-recessive years = 6.4%) *, and consumer debt now at $17.5 trillion (non-housing debt increased 63.2% over the last ten years).

In addition to traditional portfolio management and increasing loss provisions, banks can consider two additional strategies to manage credit risk:

1.Enhanced credit decisioning with alternative data: Banks can enhance their credit decisioning processes by integrating alternative data sources through open banking and fintech capabilities. This approach goes beyond traditional metrics like FICO® scores, income, and employment history, incorporating transactional data from utilities, rent, and healthcare payments. Additionally, banks can utilize insights from behavioral economics, social media, and geolocation data to refine their risk assessment strategies.

For example, Citigroup has announced two pilot programs under the Office of the Comptroller of Currency’s Project Round table for Economic Access (REACh) to extended credit to borrowers without credit making it easier for underbanked to borrow funds.

Project REACh enables banks to share this data with the three major credit bureaus — Experian, Equifax and TransUnion — which compile the credit reports that inform your credit scores. Some banks, including Chase, can already look at bank deposits and cash flow to help assess credit eligibility for consumers without a credit history.

2. Data-driven smart collections: By applying principles of behavioral economics and utilizing comprehensive data analysis, banks can develop personalized engagement strategies for collections. This method not only improves response rates but also increases the likelihood of successful outcomes. Furthermore, banks can enhance customer experience by providing easy access to payment reminders, customized payment options, and straightforward methods for scheduling and making payments.

For example, a regional bank showed a double-digit percent increase of delinquency resolution within 60 days of launch of a customized digital collection platform.

Future-proof banking: Embracing composable architecture for agile operations

For most of us, hearing about the next lunar eclipse or meteor shower with a few days’ notice is plenty of time to prepare for a proper viewing. Unfortunately, retail banks’ ability to pivot their capabilities in response to a macroeconomic event isn’t yet quite as nimble.

Several North American banks have begun to modernize their digital experiences and underlying architecture. They are moving applications and workloads to the cloud, streamlining core platforms and building integration layers. These steps are all crucial for delivery true ‘digital’ and not just ‘digitized’ banking services. Given the rapid pace of change across all industries, including banking, then a shift toward a highly composable architecture is essential to stay competitive and future-proof the business.

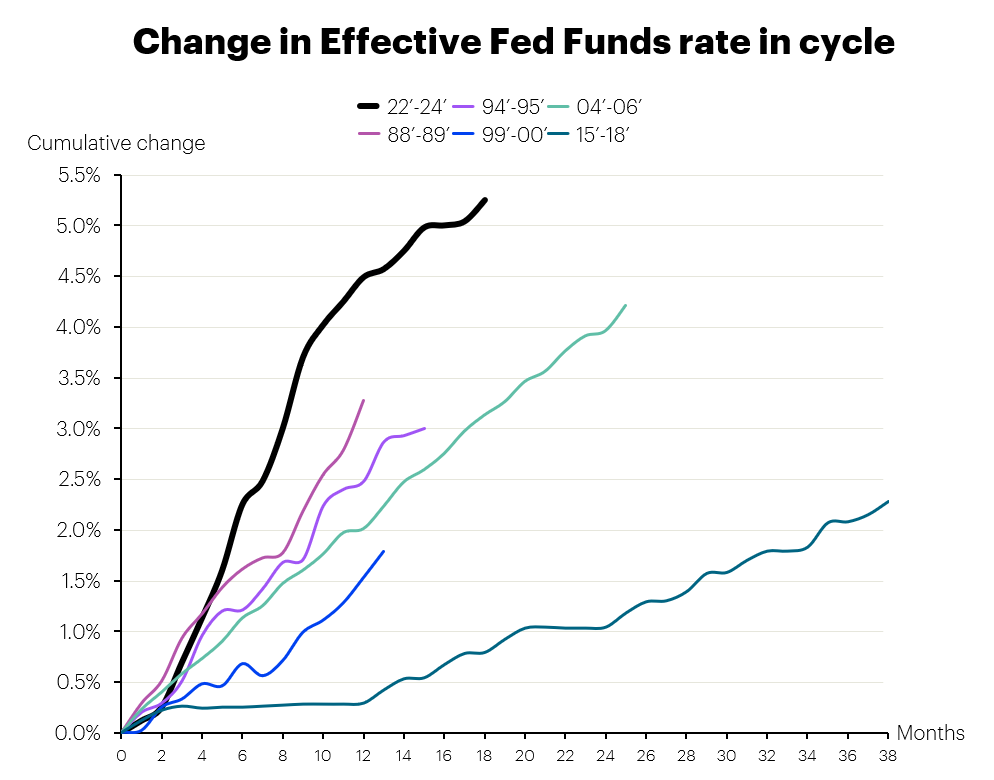

To curb inflation, the federal funds rate was increased by 525 basis points in just over 16 months: a rate of increase not seen since 1994. As rates escalated at pace, retail banks shifted their focus to deposit products for the first time in decades. However, banks efforts to manage deposit expense effectively and introduce truly innovative capabilities —without merely chasing short-term deposits—were hindered by outdated systems. These legacy systems, characterized by tightly integrated platforms, slowed down the introduction of new capabilities and made them costly.

Adopting a composable architecture becomes a ‘no regrets’ decision. Here are the advantages of a modern composable architecture:

-

- Speed to market: Reduces the lead time across infrastructure, platform and operations, enabling quicker technology deployment.

- Agility: Facilitates the swift activation of new business functions, leveraging both internal and external ‘best of breed’ partners

- Elasticity/Scalability: Enhances dynamic capacity management, including features like autoscaling and optimization, to adjust resources as needed.

- Cost Reduction: Achieves savings through the industrialization and standardization of the platform.

According to Gartner’s Hype Cycle for Digital Banking composable core banking is recognized as one of the few transformational benefits expected to reach mainstream adoption within the next 18 months.

Banking on innovation: Preparing for the “solar storm”

Banks that can stay focused on the right transformation activities, avoiding distractions like the Aurora Borealis, will be better equipped to respond to the ever-changing environment. This focus will position them to serve their customers more effectively with capabilities that are tailored to their needs, regardless of the economic or credit cycle.

For more information contact me and read our Banking Top 10 Trends for 2024.

* Source Accenture Research

This makes descriptive reference to trademarks that may be owned by others. The use of such trademarks herein is not an assertion of ownership of such trademarks by Accenture and is not intended to represent or imply the existence of an association between Accenture and the lawful owners of such trademarks.