Other parts of this series:

In our last post, we talked about how it was time for banks to start looking beyond compliance in Open Banking, or as it is enacted in Australia, the Consumer Data Right (CDR), and to imagine their role in the new application programming interface (API) and open-data economy.

Open Banking and CDR data offer banks the opportunity for greater efficiencies and new revenue growth, not to mention competitive advantages in an increasingly disrupted financial services landscape. The first step to this is moving beyond compliance as a Data Holder, which governs only the sharing of the bank’s own customer data with no monetary benefit, into ingesting CDR data in the role of an accredited Data Receiver. Then, through aggregation of their own data, CDR data and any other open data, potentially via partnerships, banks should seek insights that can fuel new products and services to be delivered through this new API and open-data ecosystem.

Then, as banks chart their CDR journeys, we see the emergence of two predominant Open Banking-powered business models.

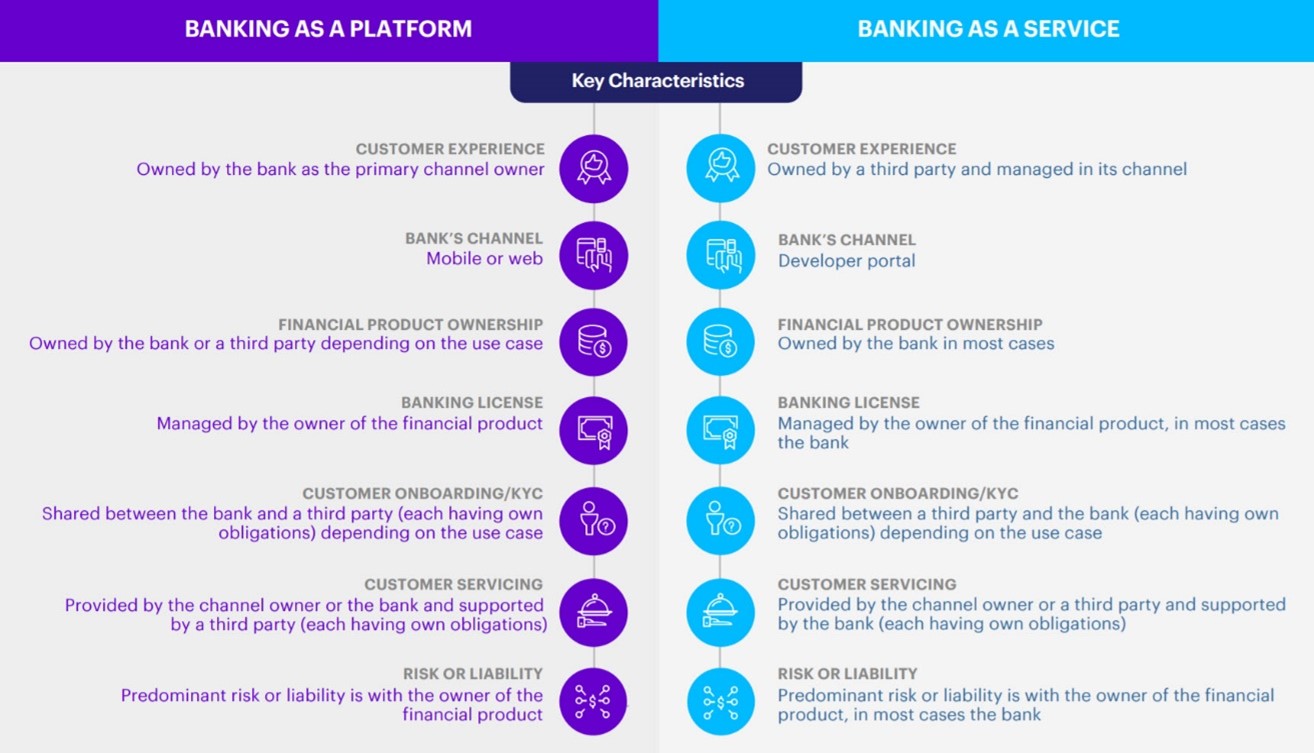

Banking as a platform

In this business model, the bank is a net consumer of partner APIs and open data—aggregating its traditional services with digital and new services from third-party partners. This model is suitable for banks that want to rapidly offer new services or expand in a new market in cooperation with ecosystem partners. It could work well for both established banks with a large customer base and a strong digital channel footprint, and new challenger banks looking to capture market share rapidly. This model helps enable banks to expand their offerings beyond financial services.

The benefits for banks include creation of revenue streams by cross- and up-selling of the new services and products and reduced costs for developing new offerings.

The benefits of this model for third parties include a wider distribution network, access to the bank’s existing customer base and the ability to bundle services with the bank’s products.

The future of banking: Time to rethink business models. An Accenture report outlines new banking business models that enable banks to reconfigure themselves to keep pace with disruption.

LEARN MOREBanking as a service

The bank is a net producer of APIs in this model. It allows banks to use APIs to distribute core financial services products such as payments, loans and mortgages. This model would best serve banks that have an efficient product manufacturing ability, strong operational processes and robust back-end capabilities. It is particularly popular within payments, credit products, treasury and transaction banking segments.

The benefits for banks include rapid expansion of distribution channels and market reach via access to new customers, and reduced operating and marketing costs for products and services.

This model benefits the third parties by generating revenue and helping attract new customers for tailored offerings.

Both models offer customers a wider range of products, improved experiences, frictionless banking journeys and customized services.

Those who are not building business models powered by Open Banking and CDR data today risk falling behind as APIs continue to emerge as a new revenue opportunity and competitive advantage in the financial services industry.

In our next post, we’ll share the monetization options for each of these emerging business models that leverage Open Banking.

For more information, read our full report on Power Plays for Monetizing Open Banking APIs.